Though we cannot accurately predict the future in detail, we can anticipate that there will be events in our lives that will be challenging. The loss of a job, home repairs such as a leaky roof or the need to replace a furnace, major car repair and medical bills are just a few examples of the financial dilemmas that families sometimes face.

Though we cannot accurately predict the future in detail, we can anticipate that there will be events in our lives that will be challenging. The loss of a job, home repairs such as a leaky roof or the need to replace a furnace, major car repair and medical bills are just a few examples of the financial dilemmas that families sometimes face.

In the paper Financially Fragile Households: Evidence and Implications, authors Lusardi, Schneider and Tufano* reported that almost half of American households stated that they would be unlikely to be able to come up with $2000 within 30 days. It can be very stressful to find ourselves without the funds to take care of our families’ needs. Using credit cards or taking out a loan may make the situation worse by adding high interest rate charges to the initial debt.

Wouldn’t it be great to reduce your family’s chances of being overwhelmed when similar situations occur? Having money in reserve allows us to be more control and provides more options in difficult circumstances. You can be better prepared to handle some of life’s challenging circumstances in the future by taking steps now to start or increase your emergency savings fund.

An emergency fund is money that you set aside in a readily accessible account specifically for unexpected events. It is an essential part of your financial plan. How much money will you need to put away? This will depend on your unique circumstances, but striving for at least six month’s worth of basic living expenses is a common goal.

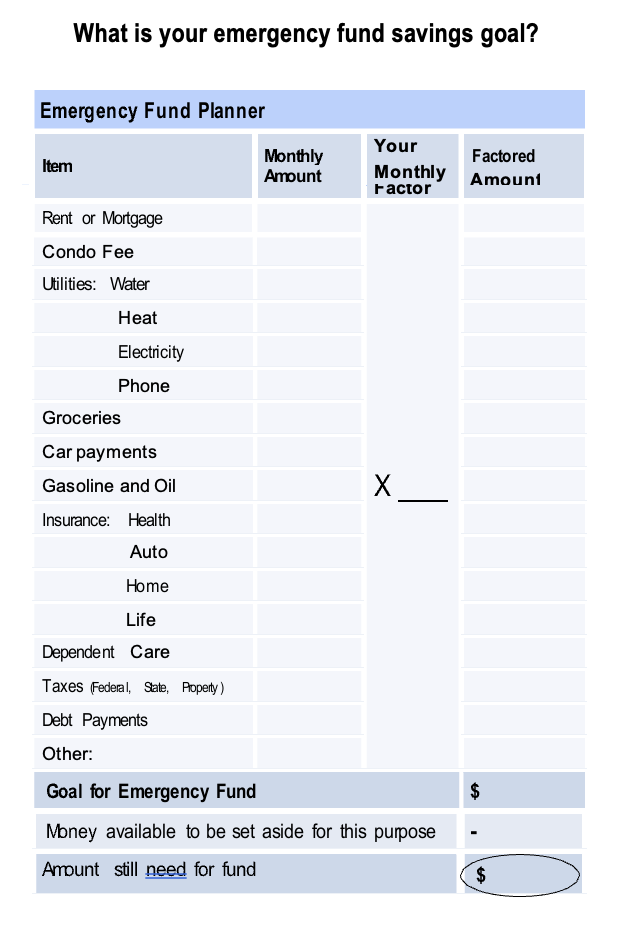

An individual who is self-employed or has an irregular income may want to set aside more over time. Basic living expenses typically include such things as a rent or mortgage payment, utilities, food, car payments, gasoline and oil, insurance, child or elder care and other debt payments. However, if that goal seems overwhelming, it may be helpful to focus first on securing one month’s worth of expenses and as that amount is reached, go on to work towards a second month’s worth and so forth. Some people may find putting a tax refund towards an emergency fund as a good way to increase an emergency fund. Setting up automatic deposits is another way to make this process easy.

What is an emergency when it comes to your personal finances? Merriam-Webster defines an emergency as “1) an unforeseen combination of circumstances or the resulting state that calls for immediate action and 2) an urgent need for assistance or relief.” This means that a great deal on a high-definition television or bargain price for a vacation by cruise ship are not likely to qualify in most situations. However, it is appropriate to use these funds when faced with circumstances such as paying a deductible to repair a roof damaged by a tree in a storm. Keep in mind that an emergency situation is really more about necessities rather than wants. Additional accounts for other family goals can be set up once the emergency fund is fully established.

What is an emergency when it comes to your personal finances? Merriam-Webster defines an emergency as “1) an unforeseen combination of circumstances or the resulting state that calls for immediate action and 2) an urgent need for assistance or relief.” This means that a great deal on a high-definition television or bargain price for a vacation by cruise ship are not likely to qualify in most situations. However, it is appropriate to use these funds when faced with circumstances such as paying a deductible to repair a roof damaged by a tree in a storm. Keep in mind that an emergency situation is really more about necessities rather than wants. Additional accounts for other family goals can be set up once the emergency fund is fully established.

Where should you keep your emergency fund? Keep in mind that you may need to access this money quickly so it needs held in an account which can be easily converted to cash.

Another important consideration is safety. The purpose of an emergency fund is to be more like insurance rather that an investment where you may choose to take some risk to achieve a higher return. It is also a good idea to confirm that such funds are federally insured through the Federal Deposit Insurance Corporation (FDIC) or the National Credit Union Administration (NCUA). As it is important that these funds be available when needed, these monies need to be in accounts with little or no risk of loss.

Starting or increasing an emergency fund provides you with a cash cushion that can help make your financial future more secure.

Use the form to the right to help you determine how much you would want to have in an emergency fund. Consider your unique circumstances and plans for the future. For example, if you are self-employed or you are expecting a baby, it would be wise to set aside a larger amount. Make adjustments to the amount to reflect your desire to work toward greater financial security.

* Lusardi, Annamaria, Daniel Schneider, and Peter Tufano. “Financially Fragile Households: Evidence and Implications.” Brookings Papers on Economic

Saving for a Rainy Day: Your Emergency Fund by Faye Griffiths-Smith, Associate Extension Educator, Family Economics and Resource Management, UConn Extension, 305 Skiff Street, North Haven, CT 06473. For more information, contact her at: faye.griffiths-smith@uconn.edu or 203.407.3160.

The University of Connecticut is an equal opportunity employer and program provider.